- HOMEPAGE

- MY STORY

- OUR SERVICES

- HIRE JESSICA TO SPEAKER

- OUR EVENTS

- FREE GUIDE

- CONTACT US

- BLOG

- Mindset & Self-Worth

- BREAKING FREE LIMITING BELIEFS

- HEALING SUPPORT: LET GO OF THE PAST

- PURPOSE ALIGNMENT: CREATE A MEANINGFUL AND FULFILLING LIFE

- SELF-LOVE UNVIELED: A JOURNEY THROUGH PHILOSOPHY, PSYCHOLOGY, AND PERSONAL GROWTH

- The Truth About Women’s Resolutions

- Mirror Talk: A 5-Minute Daily Ritual to Boost Self-Compassion

- Whose Glasses Are You Wearing?

- From Default Mode to Design Mode: Re-Wiring Your Habit Brain in Just 21 Minutes a Day

- Embracing Self-Worth: A Message to Women in Leadership

- Are You a Big Tree in a Small Pot?

- A Simple Choice for a Better Day

- Live on Purpose: A Simple System to Align Your Days with What Matters

- Mindset & Self-Worth

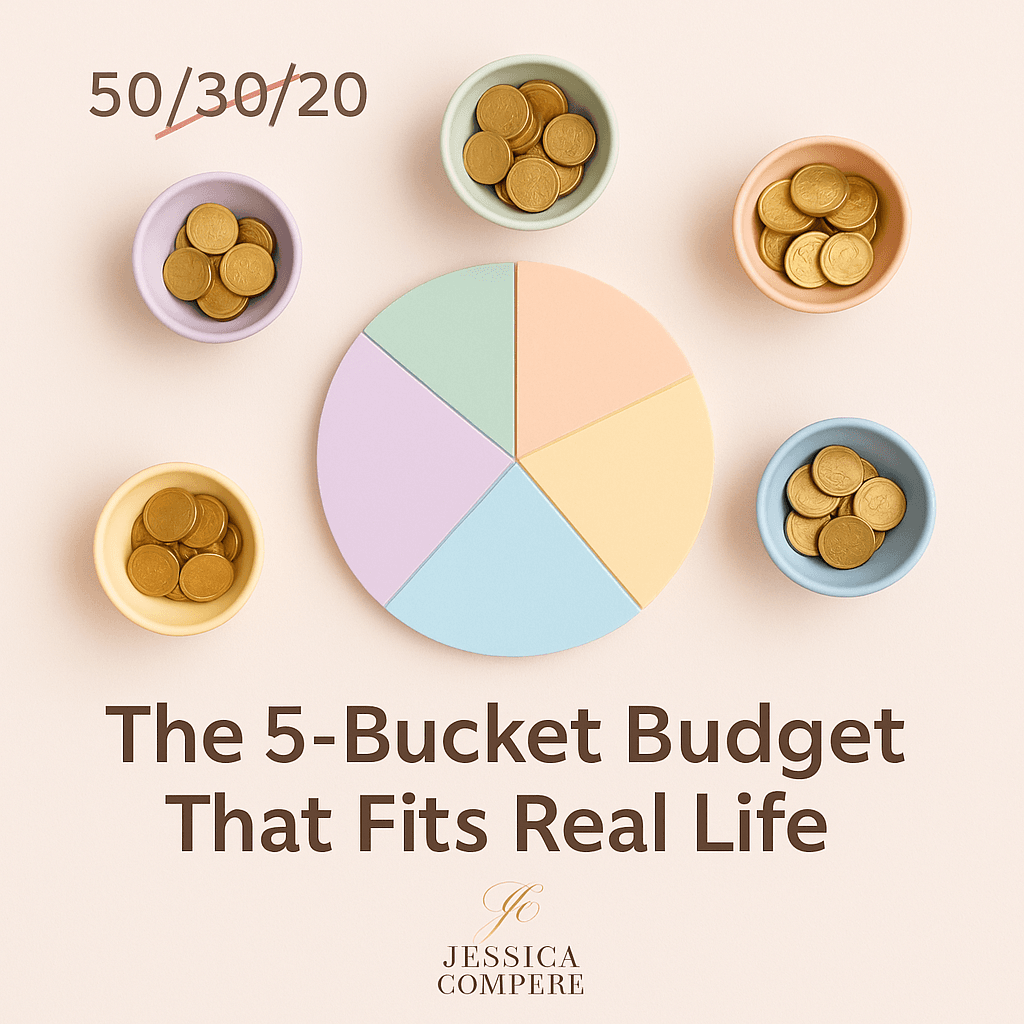

- The 50/30/20 Myth & the 5-Bucket System That Actually Fits Real Life

The 50/30/20 Myth & the 5-Bucket System That Actually Fits Real Life

- Jessica Compere. Approx. read time: 6 min

A Budget Rule Stuck in 2005

Back when cable TV still dominated and side hustles were rare, the 50/30/20 rule (50 % needs, 30 % wants, 20 % savings) felt revolutionary. Fast-forward to 2025 and that tidy split crumbles under freelance income swings, student-loan “pauses,” and groceries that cost more than a phone bill. If you’ve ever tried to shoe-horn modern life into yesterday’s math, this post is for you.

1 | Why Classic Budgets Break Down

| Old Rule | 2025 Reality | Result |

|---|---|---|

| Fixed income | Variable paychecks, gig bonuses, stock grants | Percentages swing wildly |

| One savings pot | Competing goals: emergency fund, dream trip, business capital | Priorities blur |

| “Wants” at 30 % | Uber rides + streaming + subscriptions = line-item chaos | Lifestyle creep |

The truth? Rigid ratios can make you feel like a failure even when you’re making progress.

2 | Meet the 5-Bucket System

Instead of three rigid slices, think of five flexible “buckets.” Pour money in as it arrives; siphon out when the bucket’s purpose calls.

| Bucket | Target %* | Purpose | Example Uses |

|---|---|---|---|

| 1. Essentials | 40–60 % | Keep the lights on | Rent, groceries, transport, meds |

| 2. Freedom Fund | 10–15 % | Future security | Emergency cash, debt payoff |

| 3. Joy Fund | 5–15 % | Lifestyle you feel | Dining out, hobbies, concerts |

| 4. Growth Fund | 10–20 % | Skill & wealth expansion | Courses, investing, biz tools |

| 5. Give Fund | 1–10 % | Generosity on purpose | Charities, gifts, tithes |

*Ranges let you flex with income highs/lows.

Key principle: Each dollar gets a job the moment it lands—no more “where did my paycheck go?” confusion.

3 | Step-By-Step Setup (15 min)

Open five sub-accounts (or labeled folders in your banking app).

Name auto-rules: each deposit splits by percentage into the five buckets.

Manual income? Transfer using a one-minute calculator on payday.

Review monthly: adjust ranges until they fit your real costs.

Download my Google Sheet —it calculates bucket amounts for any income.

4 | Quick Credit-Score Tune-Up

| Mini-Move | Why It Works |

|---|---|

| Set autopay for at least the minimum on every card | 35 % of FICO = payment history |

| Drop utilization below 30 % (ask for a limit raise if needed) | Low balances boost score within weeks |

| Stack due dates near payday | Prevents “oops, forgot” fees |

5 | Reflection Prompts

Which bucket feels starved right now?

How could shifting 2 % from another bucket change your stress level?

What first step could you take today—open a sub-account, set an autopay, or download the sheet?

Journal your answers; clarity follows curiosity.

6 | Mini Exercise — 24-Hour Bucket Audit

Print your last bank statement. Use five colored markers to highlight each expense by bucket. Notice where color is missing (neglected bucket) or overflowing (leaky bucket). Decide one tweak for next month.

Grab the 5-Bucket Budget Sheet—a plug-and-play Google template that auto-splits income, tracks bucket balances, and signals when it’s time to refill. Download here

Budget rules should bend to your life, not break your spirit. Swap old math for flexible buckets and watch your money finally line up with your values.

— Jessica Compere

Your Path to Empowerment · JessicaCompere.com

Join the Self-Love Circle

CONTACT JESSICA

Let's Connect!

Ready to embark on your journey of personal growth and transformation?

Whether you have questions about coaching, speaking engagements, or simply want to connect, I’d love to hear from you.

FOR FUTHER INQUIRY

+1305 - 878 - 0616

SEND US EMAIL

info@jessicacompere.com